LIFE INSURANCE

Would you do away with life insurance? Do you think it’s OK to NOT have life insurance? If you do, you are probably one of the 0.001% of the populace who thinks so. Jokes apart, there are no two ways about the fact that life insurance is a must-have financial product for everyone.

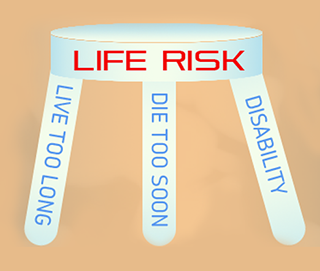

Life Insurance provides a lump sum benefit payable upon your death, to your next of kin. Most life insurance policies are term life insurance policies as the contract is only renewable for a certain term. Typically, all term life insurance policies have the age limit of 65 years, beyond which, the policy can no longer be renewed.

Beneficiaries of life insurance policies are normally your dependants. Life insurance can be used to pay back debts, future liabilities/expenses and/or provide an income stream for the dependents. In essence, it helps to keep your family’s financial plans on track and maintain their current lifestyle.

How much life insurance is necessary?

Although, it is not possible to attach a rupee value to human life, it is nonetheless important for you to estimate the economic value of your life in terms of what it will take for your family members to be financially independent in your absence. In insurance parlance this is the sum assured and the financial estimate of the value of your life is called Human Life Value (HLV).

HLV is calculated in two steps:

Life Insurance cover should include:

The amount of Life Insurance cover required is reduced by:

Although insurance policies are a necessary part of your overall financial plan, it is important to remember:

Health &Allied insurance

Insurance cover is not limited to only life or term insurance. It can be extended to other assets like property, vehicles or other facets of life like healthcare management.

What is Health Insurance?

Health insurance is an insurance product which covers medical and surgical expenses of an insured individual. It reimburses the expenses incurred due to illness or injury or pays the care provider of the insured individual directly.Based on the terms of insurance coverage, either the insured person pays healthcare costs out-of-pocket and is subsequently reimbursed, or the insurance company reimburses costs directly to the hospital (cashless insurance).

Need for Health Insurance

Medicare or medical costs increase, year-on-year. As a matter of fact, inflation in medicare is higher than inflation in food and other articles of daily use. Typically, while inflation in food and clothing is in single digits, medicare costs usually escalate in double digits.

For an individual who hasn’t saved enough money, arranging for funds to pay for healthcare at the eleventh hour can be a huge challenge. This is particularly daunting for seniors, given that most serious ailments strike at an advanced age.

One way to provide for health-related / medical emergencies is by investing in health insurance. Health insurance offers considerable flexibility in terms of disease and chronic illness coverage. For instance, some health insurance plans cover as many as 30 critical illnesses and over 80 surgical procedures.

Ideally, medical insurance plans are are expected to disburse the payment towards surgery/illness regardless of actual medical expenses. Health insurance policies continue even after the benefit payment on selected illnesses, has been issued.

With health insurance, you are assured of a more secure future both health-wise and money-wise. This makes health insurance policies critical for individuals, especially if they are responsible for the financial well-being of the family.

Allied health plans include accidental & critical care policies

KEY MAN INSURANCE

Why is key man insurance needed?

All businesses should consider the use of insurance to compensate the business for any financial loss or cost suffered because an undesirable life event has occurred with respect to a key person. Most businesses take out insurance cover for assets that do not make them profits – their plant, equipment, vehicles and buildings. However, the human assets that, through initiative, drive, skill, specialist knowledge and ingenuity that can turn the capital and assets into a profit, are highly valuable to the business as well. Hence, keeping some money aside for ‘Key Man’ insurance, is a good strategy to cover for the loss of productivity, if there is an untoward incident involving the key man (men) of the business.

Who is a Key man?

A 'key man' is a company executive (Man or Woman) whose continued association with the business provides that business with a significant and direct economic gain. Economic gain means more than just profits. It can, amongst other things, also include cost savings, capital injections, good will, access to credit and access to customers. A common example of a key person is an employee who is directly responsible for bringing in sales or who holds the key technical expertise on which a business relies. The owners of the business will usually be key people. A key person could also include "top level management" people in the organisation namely

How much should ‘Key Man’ insurance coverage be?

Key man insurance should compensate the business for the loss of two different qualities.

Key man insurance proceeds can replace the lost profit or capital value that the key person would have generated. The insurance funds can be used to stabilise the business until a suitable replacement person is employed. The replacement person is usually skilled to the same degree as the lost employee or is capable of being trained to have the same key skills. Key man insurance proceeds can bridge the gap and enable the business to operate efficiently through, and after, the replacement ordeal.

Losing a key man can cause revenues to go down, and business costs to increase. In such cases, the funds set aside as key man insurance can be used to mitigate the rise in business costs, in order to achieve stability.

Only term insurance policies are allowed under "KEY MAN INSURANCE".

Investor Login

Investor Login